| << Chapter < Page | Chapter >> Page > |

By the end of this section, you will be able to:

First let’s first focus on what economists mean by demand, what they mean by supply, and then how demand and supply interact in a market.

Economists use the term demand to refer to the amount of some good or service consumers are willing and able to purchase at each price. Demand is based on needs and wants—a consumer may be able to differentiate between a need and a want, but from an economist’s perspective they are the same thing. Demand is also based on ability to pay. If you cannot pay for it, you have no effective demand.

What a buyer pays for a unit of the specific good or service is called price . The total number of units purchased at that price is called the quantity demanded . A rise in price of a good or service almost always decreases the quantity demanded of that good or service. Conversely, a fall in price will increase the quantity demanded. When the price of a gallon of gasoline goes up, for example, people look for ways to reduce their consumption by combining several errands, commuting by carpool or mass transit, or taking weekend or vacation trips closer to home. Economists call this inverse relationship between price and quantity demanded the law of demand . The law of demand assumes that all other variables that affect demand (to be explained in the next module) are held constant.

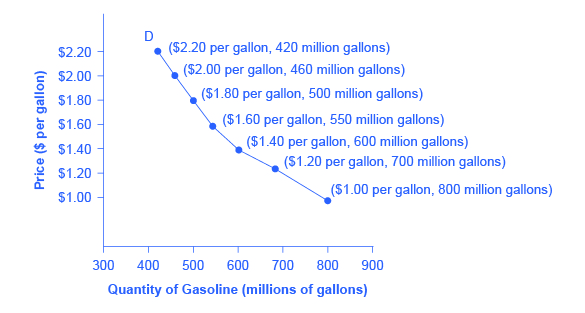

An example from the market for gasoline can be shown in the form of a table or a graph. A table that shows the quantity demanded at each price, such as [link] , is called a demand schedule . Price in this case is measured in dollars per gallon of gasoline. The quantity demanded is measured in millions of gallons over some time period (for example, per day or per year) and over some geographic area (like a state or a country). A demand curve shows the relationship between price and quantity demanded on a graph like [link] , with quantity on the horizontal axis and the price per gallon on the vertical axis. (Note that this is an exception to the normal rule in mathematics that the independent variable (x) goes on the horizontal axis and the dependent variable (y) goes on the vertical. Economics is not math.)

The demand schedule shown by [link] and the demand curve shown by the graph in [link] are two ways of describing the same relationship between price and quantity demanded.

| Price (per gallon) | Quantity Demanded (millions of gallons) |

|---|---|

| $1.00 | 800 |

| $1.20 | 700 |

| $1.40 | 600 |

| $1.60 | 550 |

| $1.80 | 500 |

| $2.00 | 460 |

| $2.20 | 420 |

Notification Switch

Would you like to follow the 'Openstax microeconomics in ten weeks' conversation and receive update notifications?

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|